- Activant's Greene Street Observer

- Posts

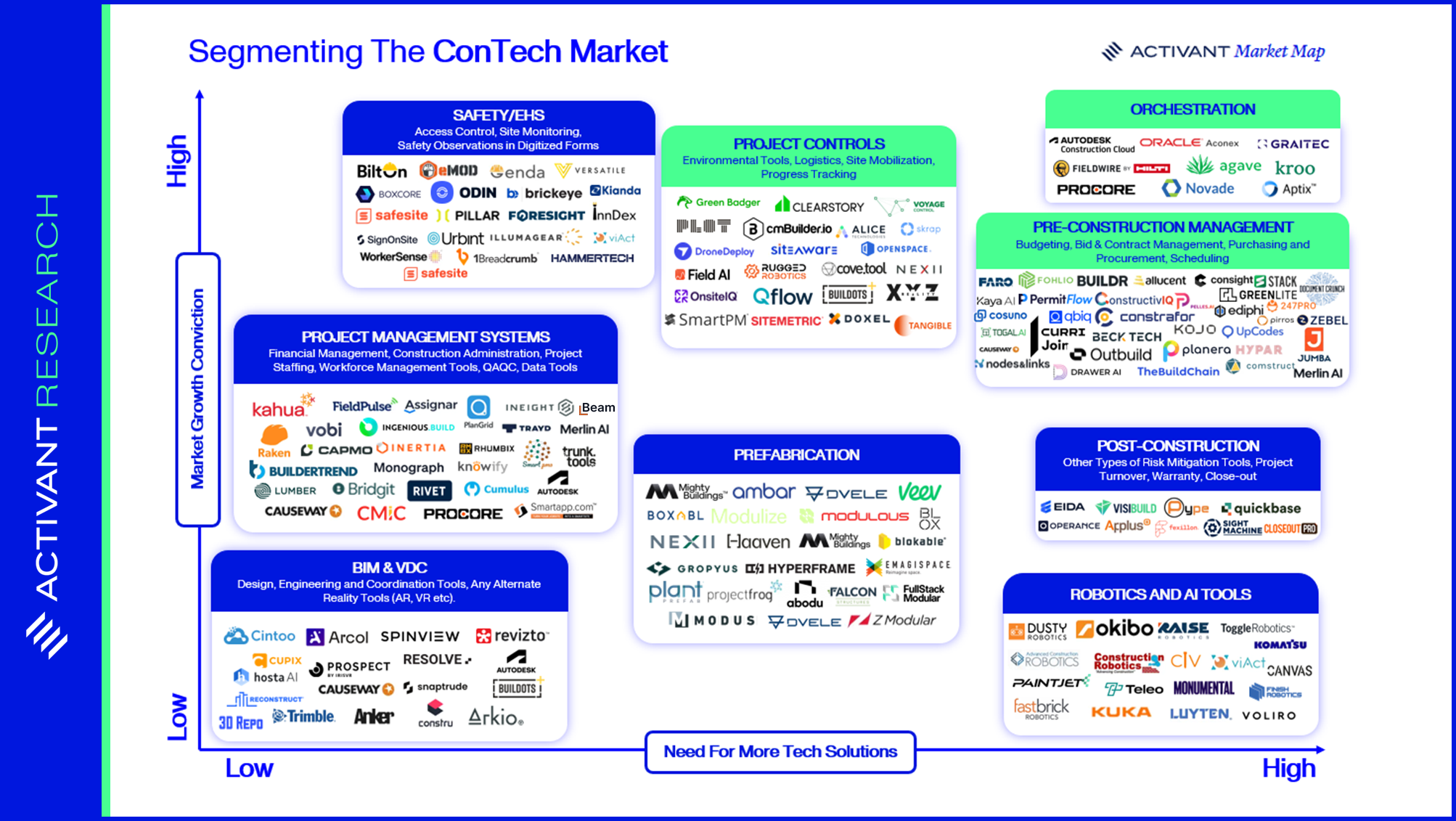

- Breaking Ground:

Breaking Ground:

Addressing Construction’s Productivity Challenge

Rebecca Rodseth

April 01, 2025

Introduction

From skyscrapers to bridges, construction is responsible for building the infrastructure that underpins modern society. The industry makes up 14% of global GDP and is expected to have a global spend of $15 trillion in 2030. The task seems simple enough: build under budget, on schedule, and safely. However, construction workflows are highly inefficient and outdated. We believe this is strongly correlated to the fact that midsize construction companies allocate only 1.4% of their revenue to IT, a stark contrast to industries like industrial manufacturing that spends 2.3% and utilities that spends around 4.2%.

But it’s not all doom and gloom. This highly complex and dynamic industry also presents a significant opportunity. Global building floor space is on track to double by 2060 – the equivalent of adding an entire New York City every month for 40 years. Meeting this surging demand for infrastructure and housing, amid chronic labor shortages (in developed markets) and rising cost pressures, will require a technological revolution in construction. Construction Technology (ConTech) startups looking to shake up the status quo are slowly gaining traction. These innovative companies offer digital tools, software, and solutions to address the major challenges faced by construction companies seeking to modernize and harness technology to dramatically improve efficiency.

Construction’s Productivity Woes

The construction industry has been caught in a productivity rut. From 2000 to 2022 productivity in the industry improved by only 10%, while the broader economy saw a 50% gain and the manufacturing sector delivered a 90% improvement. We believe that there are four key challenges underpinning this poor productivity performance:

1. Construction has a fragmented ecosystem that makes unified tech adoption challenging. There are multiple stakeholders (contractors, subcontractors, suppliers, architects, engineers, clients) involved in each project and it is often difficult to relay information from one party to the next. Miscommunication and poor project data accounts for 48% of all rework on U.S. construction job sites, costing the industry over $31 billion annually.

2. The ageing construction workforce has historically been resistant to changing established analog processes. Research shows that 45% of construction workers are over the age of 45 and that these old school leaders are risk-averse and hesitant to embrace new technology and the inevitable implementation challenges that typically arise.

3. This is compounded by the lack of spending on technology in the industry. We noted above that the industry only spends an average of 1.4% of revenue on technology; manual data collection and data entry are still common on construction sites, despite increased stakeholder pressure for data transparency, integration and real-time decision-making.

4. Industry margins are tight, particularly for the smaller contractors in the long tail where ~68% businesses have fewer than five employees. Construction material price increases of 11.2% in 2023 and 10.3% in 2022 have eaten into profit margins and increased the pressure to remain competitive. The shortage of skilled workers, particularly in the residential sector where attrition rates are higher and 90% of U.S. construction companies claim to be unable to find sufficient skilled workers, has driven up the cost of labor. Additional pressure on margins has been driven by supply chain disruptions that have become all too common over the past few years, with an estimated ~75% of projects finishing over time and over budget.

Despite these challenges, and in many cases specifically to address them, change is coming. Evolving industry dynamics are forcing the construction industry to lean into tech adoption. This transition is being supported by:

· Regulation and government funding in place to support ConTech: There are currently many challenges to historical U.S. government funding allocations, but the Infrastructure Investment and Jobs Act (IIJA) allocated $100 million to ConTech over the next five years. Additionally, the Advanced Digital Construction Management Systems (ADCMS) Grant Program, administered by the Federal Highway Administration, offers up to $5 million in grants. Similar regulations have also been introduced in Europe to incentivize or mandate the use of ConTech tools. These include the UK’s new Building Safety Act which mandates a digital “golden thread” of building data for new projects, and Sweden’s ID06 system which now requires digital IDs for all construction workers on site.

· Client demand: Activant’s expert interviews highlighted that there is almost always some sort of mandate for technology from the client side. Requests-for-proposals (RFPs) often specifically require a description of the use of technology when bids are submitted, and almost every project has a mandate to use a web-based project management platform.

· Increased competition in the market: Innovation and digital tools give contractors a competitive edge in the field and in the tender process. Experts estimate that construction companies investing in digitization and embracing new materials and advanced automation could see a 50%-60% increase in their overall productivity. This could be a huge competitive differentiator.

· Changing management landscape: The retirement of experienced construction workers is accelerating the industry’s embrace of technology. Younger, tech-savvy generations are more open to digital tools and have seen how solutions such as Procore have been able to add real value. Digital transformation is now a priority for 72% of construction companies worldwide.

While these tailwinds are increasing technology adoption, the process is slow and there is a long way to go. We are, however, optimistic that the industry has recognized the need for change and the impact that digital tools can deliver.